Year-end Tax Insights!

Mission Wealth Market Update 6/7/2022

Market Update

2022 has so far been marked by a decided uptick in volatility. Concerns surrounding inflation, rising interest rates on the back of Fed policy, Russia’s invasion of Ukraine and more recently, increased concerns about an economic slowdown, have all led to investor uncertainties. Further complicating matters and confounding some has been a recent dynamic of good news is bad; bad news is good, whereby the market reacts positively to the release of weaker economic data and reacts negatively to stronger economic data. The prevailing view being that weaker economic data may lead to the Fed slowing the speed of its rate hiking cycle. While it has been a challenging start to the year for public stocks and bonds, select income-oriented strategies have performed well. Moreover, our outlook for stocks and bonds has become much more constructive. On a forward-looking basis, we believe current levels may present an attractive entry point.

Overview

- The start of the year has been marked by a notable increase in market volatility; however, we believe that current levels may present an attractive entry point for investors.

- Market disruptions have led to enhanced portfolio opportunities, including rebalancing and tax-loss harvesting.

- We believe the current market sell-off isn’t reflective of underlying fundamentals, and concerns about a near-term recession are overdone. However, there is a risk overhang with persistent inflation.

- Our long-term outlook remains favorable for stocks, and we believe current levels offer upside potential.

- We believe bond returns will primarily be driven by current yields, while select income-oriented strategies may perform well under the current macroeconomic environment.

- We believe our portfolios are well positioned to navigate the forthcoming period and will continue to meet the long-term goals of our clients providing exposure to long term growth and current income.

Volatility: A Consequence of Reduced Accommodation

Ahead of 2022, we had expected a rise in volatility as the market transitions back towards a more “normal” market environment less influenced by accommodative policies. Our thoughts go out to all those affected by the devastating conflict in Ukraine and Mission Wealth is actively supporting non-profit organizations focused on the humanitarian effort. While Russia’s invasion came as a shock and led to an increase in market volatility, we had nonetheless anticipated a rise in volatility consistent with historic norms as historically large accommodative policies are being taken away. The size and scope of accommodative policies pursued globally to address the COVID pandemic dwarfed any similar instance historically, and arguably acted as a tailwind for the stock market in the aftermath of the COVID-driven March 2020 sell-off, while also containing volatility. Now that those unprecedentedly large accommodative policies are being unwound, it is understandably causing some market disruptions.

Enhanced Opportunities

Current market disruptions have caused divergence in performance across asset classes and has led to increased opportunities across our portfolios. We continue to maintain our disciplined approach to portfolio rebalancing, which helps strip out short-term headline noise and focus on long-term fundamentals. This disciplined approach forces us to “buy low, sell high” and particularly during times of increased market dislocation, may prove beneficial for overall performance. For instance, we had been trimming U.S. Growth stock exposures in favor of Value stocks towards the end of 2021 based on relative performance at the time. Value stocks have since outperformed in 2022. Now, we are taking the opportunity to add to Growth stocks on weakness, where underweight and appropriate. Similarly, we had increased exposures to select income-oriented strategies ahead of the Fed raising interest rates and with a backdrop of elevated inflation and above-trend economic growth, which we believed would be favorable for these strategies, and which has been borne out so far this year. We have also tactically tax loss harvested across taxable client accounts, taking advantage of select asset class weakness to ultimately enhance the after-tax returns for our clients.

Uncertainty Overdone

Notwithstanding our view that an increase in volatility was a natural byproduct of the Fed and the Treasury taking away historically large accommodative policies, the extent of this year’s market movement doesn’t appear consistent with the underlying economic fundamentals. Only 1932 (Great Depression), 1940 (World War II), and 1970 (the Vietnam War and a recession) had worse starts to the year for the stock market. We certainly don’t anticipate a significant recession (though risks exist) – let alone a depression – in the foreseeable future, while Russia’s invasion of Ukraine – which unfortunately appears likely to be a prolonged conflict – is unlikely to spiral into a wider war outside of the region.

Regarding the economy, we believe concerns about a near-term recession are overdone: consumers remain very healthy and continue to be supported by a strong labor market. Corporate and consumer balance sheets remain robust. The consensus forecast for 2022 real GDP growth is currently +2.8% (vs. long term trend growth of ~2%) and +2.1% for 2023. Importantly, of all 66 estimates for 2022 growth and of all 61 estimates for 2023 growth included in FactSet coverage, not one forecaster expects a recession in either 2022 or 2023.

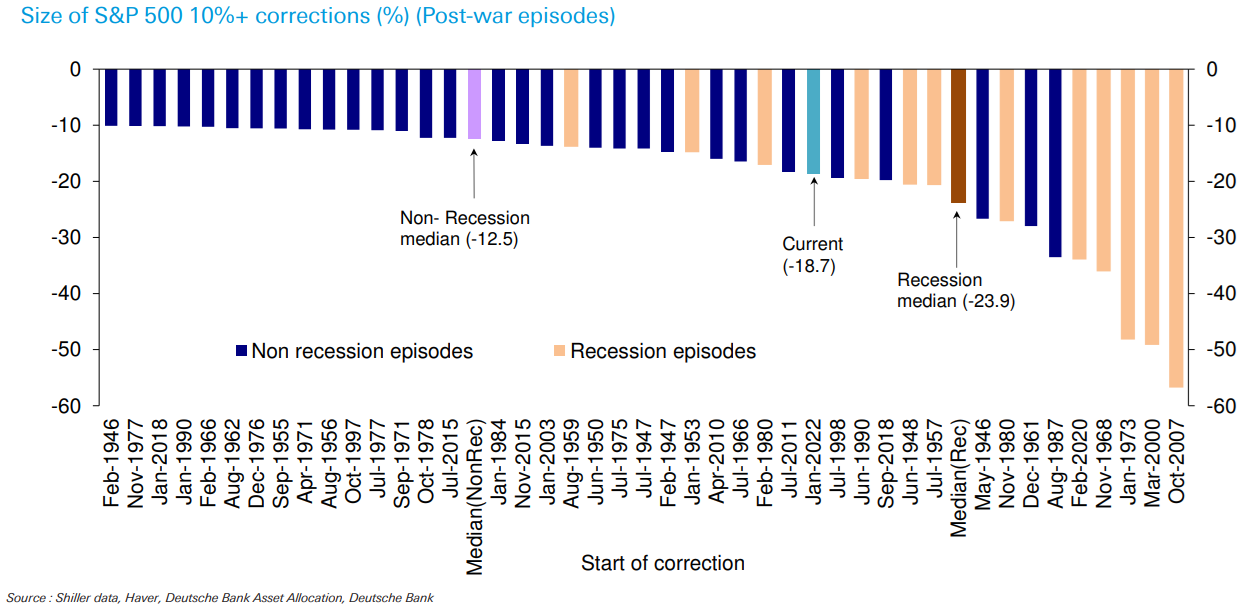

Through the market bottom in May, the S&P 500 was down -18.7%. For context, the median non-recession driven market sell-off in the post WWII era has been -12.5%. The median recession-driven market correction over the same timeframe has been -23.9%. While economic forecasts for real GDP growth have been revised lower, our base case is for above trend economic growth through this year and into 2023, yet the market has reacted as if a recession is imminent.

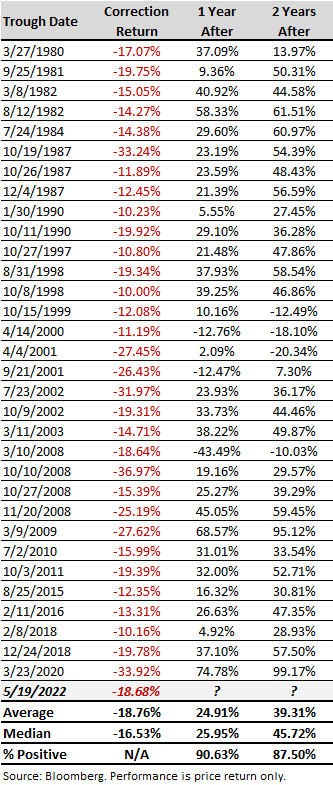

Positive Upside Potential for Stocks

With this backdrop, we are constructive on the outlook for the stock market. In past instances of market corrections, the subsequent 12-month and 24-month returns have historically and on average – been very strong.

Bonds: Pain Behind Us

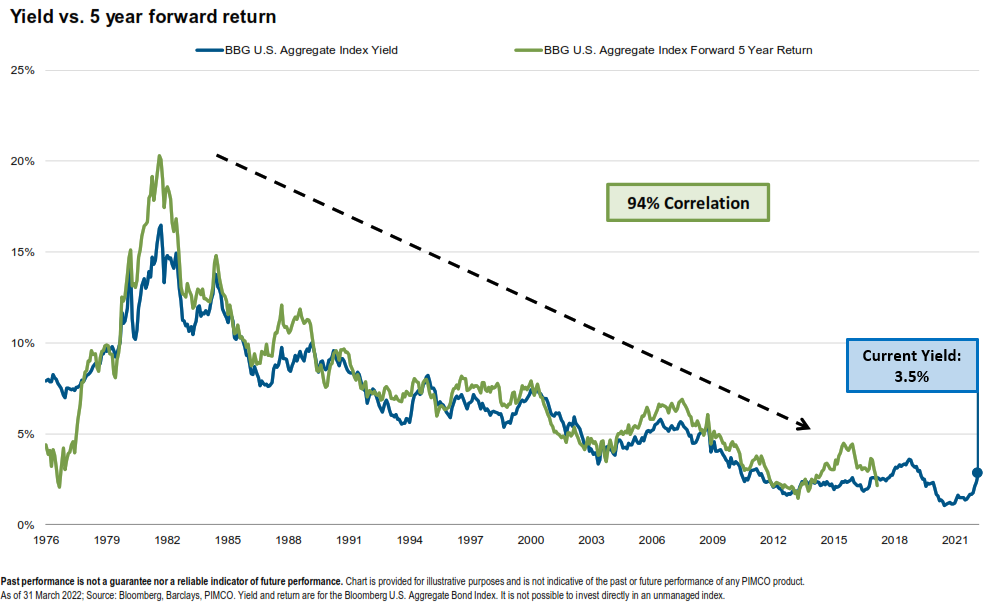

After experiencing a significant move higher to begin the year, we believe bond yields are entering range-bound territory with the benchmark 10-Year Treasury yield likely to trade in the +/-3% level. As such, and moving forward, the returns for high quality bond allocations are likely to be primarily driven by the current yield on a bond portfolio, with limited capital appreciation/depreciation. To this end, the current yield to maturity on the broad bond market (Bloomberg Aggregate Index) is 3.5%, and many of our preferred bond holdings yield north of that. The importance of yield for the bond market cannot be overstated: the current yield is the single largest determinant of future returns. Indeed, the correlation between current yield and subsequent five-year returns for the Bloomberg Aggregate Index is 94%.

Speaking of yield, we continue to favor allocations to select income-oriented strategies such as floating rate securities, real estate, and direct credit, all of which we believe will perform well with a backdrop of elevated (but falling) inflation, above-trend economic growth and rising interest rates.

Overall, we believe our portfolios are well positioned to continue to meet the long-term financial goals of our clients.

For additional information, please don’t hesitate to contact your Client Advisor.

ALL INFORMATION HEREIN HAS BEEN PREPARED SOLELY FOR INFORMATIONAL PURPOSES. ADVISORY SERVICES ARE ONLY OFFERED TO CLIENTS OR PROSPECTIVE CLIENTS WHERE MISSION WEALTH AND ITS REPRESENTATIVES ARE PROPERLY LICENSED OR EXEMPT FROM LICENSURE. PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RETURNS. INVESTING INVOLVES RISK AND POSSIBLE LOSS OF PRINCIPAL CAPITAL. NO ADVICE MAY BE RENDERED BY MISSION WEALTH UNLESS A CLIENT SERVICE AGREEMENT IS IN PLACE.

MISSION WEALTH IS A REGISTERED INVESTMENT ADVISER. THIS DOCUMENT IS SOLELY FOR INFORMATIONAL PURPOSES, NO INVESTMENTS ARE RECOMMENDED.

00452817 06/22