Year-end Tax Insights!

Mission Wealth Market Update 5/1/24

In

/

by Kieran Osborne, MBus, CFA®, Chief Investment Officer

/

May 1, 2024

Market Update Key Takeaways

As expected, the Fed held rates steady and is likely to wait longer before making its first rate cut, while Fed Chair Powell indicated rate hikes are all but off the table, at least over the near term. What this means for our investment portfolios:

- Upwardly revised economic growth and sticky inflation may underpin a “higher for longer” interest rate environment.

- We expect a moderation in long-term returns for stocks.

- Bond yields are attractive, and we maintain a diversified exposure as appropriate.

- Alternative assets may offer enhanced risk-adjusted long-term returns.

Fed Holds Rates Steady

As was widely anticipated, the Fed held rates steady at its May 1st FOMC meeting, maintaining the target range for the fed funds rate at 5.25% – 5.50%. The accompanying statement noted that economic activity continues to expand at a solid pace, while the labor market remains strong. Inflation has eased but remains sticky and above the Fed’s goal, with the statement noting that in recent months “there has been a lack of further progress toward the Committee’s 2% inflation objective.” Moreover, the statement indicated the Fed believes it will not be appropriate to cut interest rates “until it has gained greater confidence that inflation is moving sustainably toward 2%.” However, the Fed did announce it intends to scale back its quantitative tightening (QT), by slowing the pace of decline of securities held on its balance sheet (reduction of Treasury securities will slow from $60 billion to $25 billion per month).

Wait-and-See Approach

We’ll have to wait until the next FOMC meeting in June for the Fed’s updated economic projection materials, aka “dot plot” forecasts, so all eyes were on Fed Chair Powell’s subsequent press conference for any hint of changes to the outlook for monetary policy. Key takeaways from the press conference included an indication that the Fed is likely to wait longer before making its first rate cut, while rate hikes are all but off the table, at least over the near term. Powell indicated it may take longer than expected to gain confidence that inflation will return to target and that the Fed is cautious about cutting rates too early. Powell also stated that it is unlikely the next policy rate move would be a hike, though he did hedge himself somewhat by reiterating the data-dependency of monetary policy. In essence, the Fed is adopting a wait-and-see approach.

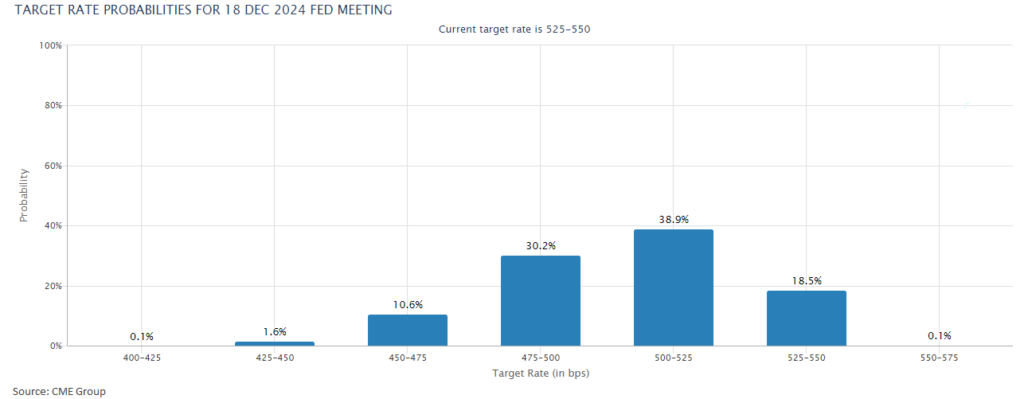

Market Expects More Moderate Rate Cuts

Recently, hotter inflation data and today’s Fed decision continue to underpin a “higher for longer” interest rate narrative. As recently as the end of 2023, the market had anticipated up to six 0.25% Fed rate cuts. As of writing, the market now anticipates one or two 0.25% rate cuts for the year, and assigns a nearly 20% chance the Fed does not cut rates in 2024:

Upward Revisions to the Economy and Inflation

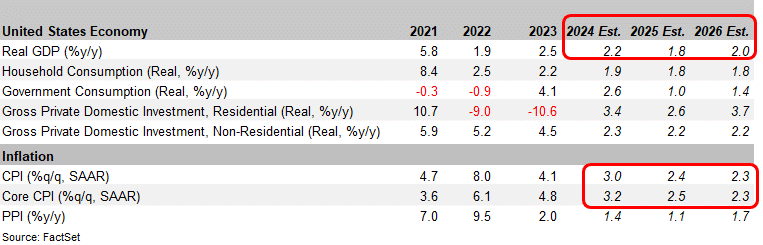

As the economy has improved and economic data has come in ahead of expectations, economic growth expectations have consistently been revised higher. The current expectation for GDP growth for 2024 stands at 2.2%, marginally higher than the long-term trend growth rate of ~2%. For context, at the beginning of the year, the market expected 2024’s economic growth to come in at 1.2%. Moreover, inflation is expected to stay higher and above the Fed’s goal of 2% at least through 2026.

With this backdrop, we believe the Fed will be hesitant to cut rates too quickly and will take a cautious approach to any future rate cuts. All of this underpins our view that we have already entered a structural shift towards tighter monetary policy, and we will experience a higher for longer interest rate environment.

Investment Implications

We expect a moderation in long-term returns for the stock market. We’re not bearish on the outlook for stocks, we simply think that given the shift towards tighter monetary policy in the years ahead that annualized return expectations over the long haul need to be more aligned with historic averages of mid to high single digits. Bond yields are a lot more attractive today relative to recent years, with many of our preferred bond funds yielding mid to high single digits. At the same time, the robustness of the economy has helped the underlying fundamentals of many bond credits. We have high conviction in alternative asset classes, which we believe may generate enhanced risk-adjusted returns and attractive income streams in the years ahead, with less correlation to public markets.

Ultimately, we believe our portfolios are well-positioned to navigate the current environment and continue to achieve the long-term financial goals of our clients.

Customized Investment Management Solutions

At Mission Wealth, we develop customized, globally diversified, tax-efficient portfolios tailored to your financial plan and built to stand the test of time. Contact us below for a free portfolio review.Get Started Today

Investment Advice Fit For Your Needs

At Mission Wealth, we are deeply rooted in an evidence-based investment strategy built on decades of Nobel Prize-winning research. We ignore the media noise and Wall Street hype, relying instead on a long-term approach and proven principles that reward investors over time. For more information on Mission Wealth's investment strategies, please visit missionwealth.com.

To meet with a Mission Wealth financial advisor, please contact us online today or call us at (805) 882-2360.

Mission Wealth is a Registered Investment Advisor. This commentary reflects the personal opinions, viewpoints, and analyses of the Mission Wealth employees providing such comments. It should not be regarded as a description of advisory services provided by Mission Wealth or performance returns of any Mission Wealth client. The views reflected in the commentary are subject to change at any time without notice. Nothing in this commentary constitutes investment advice, performance data, or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Mission Wealth manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

MISSION WEALTH IS A REGISTERED INVESTMENT ADVISOR. ALL RIGHTS RESERVED. 00595317 05/24

Let's Keep in Touch!

Subscribe for exclusive content and timely tips to empower you on your financial journey. Our communications go straight into your inbox, so you'll never miss out on expert advice that can positively impact your life.Recent Investment Insights Articles

Market Update 3/9/26

March 9, 2026A closer look at current global events, market volatility, and how diversified portfolios and long-term strategies can help navigate uncertainty....

Market Update 3/2/26

March 2, 2026Markets have weathered wars and global conflict before. Learn why history supports long-term resilience and disciplined investing during volatility....

Market Perspectives Q1 2026

February 25, 2026Quarterly insights from Mission Wealth on market trends, AI impact, economic growth, and strategies to help investors make informed financial decisions....