Year-end Tax Insights!

What Is the Capital Stack? How Investment Risk Changes from Debt to Equity

Short Answer: The capital stack determines who gets paid first in an investment. Investors higher in the stack (like senior debt) typically face lower risk and higher recovery rates, while those lower in the stack (like equity) take on more risk but have greater upside potential.

When people invest in a company, whether through stocks, bonds, or loans (debt), they’re participating in what’s known as the capital stack. This determines where the investor stands regarding who gets paid first, who bears the most risk, and how likely each layer is to suffer losses, especially during downturns or defaults.

Understanding the capital stack is critical because not all debt and equity investments carry the same level of protection or risk exposure.

What Is the Capital Stack?

The capital stack is the hierarchy of a company’s obligations to investors:

Contractual Repayment Rights:

- Senior Secured Debt (least risk)

- Senior Unsecured Debt

- Subordinated/Junior/Mezzanine Debt

- Preferred Equity

No Repayment Rights:

5. Common Equity (most risk)

As you move down the stack, risk generally increases, and the likelihood of loss rises, but potential return may also increase.

The Capital Stack Layers Explained

First Position (1st): Senior Secured Debt (Top of the Stack) – 97% of CCFLX loans are in this position (learn more from the fact page).

- Lowest default risk within a company’s structure.

- First to be repaid.

- Often secured by assets.

- Layers of Senior Debt

- First-lien – usually backed by specific assets (real estate, equipment, inventory, accounts receivable, etc.).

- Second-lien – also secured (aka asset-based lending).

Historical context:

Even when companies default, senior lenders often recover a meaningful portion of their capital. In many cases, if senior lenders are not made whole, investors below them in the stack may lose their entire investment.

What this means for investors:

- Lower probability of permanent loss compared to other ownership positions.

- Often attractive during uncertain economic periods.

- Losses in diversified portfolios tend to be partial rather than total.

Investors sometimes refer to shifting from equities to senior debt as “moving up the capital stack” to reduce risk exposure.

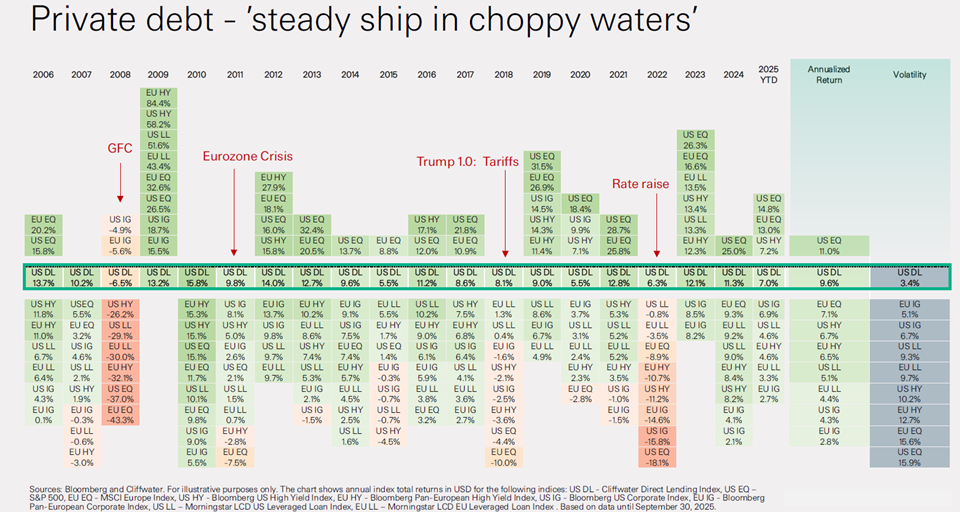

Another way to evaluate risk is by comparing income spreads. For example, if U.S. Treasuries yield 3.5% and another debt investment yields 8%, the investor earns an additional 4.5% to compensate for risk. That extra yield can absorb some level of defaults before the investment underperforms safer alternatives. Historically, default rates for senior secured loans have been well below that spread, especially after factoring in recovery rates.

The chart below shows that high-yield bonds are widely accepted as a core staple of diversified portfolios, yet their default rates have historically been higher than those of senior direct lending and leveraged loans.

Second Position (2nd): Senior Unsecured Debt

- Paid after the senior (first-position) debt is made whole.

- Usually, a general creditor is not specifically secured by a corresponding asset already pledged above.

- Receives a higher interest rate than first-position investors.

Default reality:

- More exposed in downturns.

- Recovery rates are lower than those of senior first-lien debt.

Third Position (3rd): Subordinated (Junior) Debt

- Paid after senior secured and unsecured debt is made whole.

- Receives a higher interest rate than first and second-position investors.

- This category includes high-yield bonds and mezzanine (bridge) financing.

Default reality:

- More exposed in downturns.

- Recovery rates are lower as others higher in the stack are paid off first.

Positions 1-3 become equity owners upon default.

Fourth Position (4th): Preferred Equity

- A hybrid of debt and equity.

- Paid after all debt holders are fully satisfied.

Default reality:

- Often wiped out in restructurings.

- No guaranteed recovery.

What this means for investors:

- Income potential, but fragile in distress.

Fifth Position (5th): Common Equity (Stocks)

- Last in line to be paid.

- Last in line in case of distress.

- Highest upside, highest risk.

Default reality:

- In most bankruptcies, equity goes to zero, and the debt holders (above) become the owners.

What this means for investors:

- You’re betting on growth, no protection.

The Capital Stack Bottom Line

Default risk is not evenly distributed—it increases meaningfully as you move down the capital stack.

-

Higher in the stack = greater protection, lower volatility

-

Lower in the stack = higher growth potential, greater loss exposure

While no investment is risk-free, understanding where an investment sits in the capital structure can help investors make more informed, strategic decisions.

A well-constructed portfolio often includes exposure across multiple layers of the capital stack, balancing income, growth, and risk management.

The historical data below help illustrate how position in the capital stack can influence outcomes during periods of market stress. As shown in the chart, investments higher in the capital structure, such as senior direct lending, have historically demonstrated more resilient performance during market dislocations compared to lower-ranking debt and equity investments.

Frequently Asked Questions

1. Why is senior debt considered safer than equity?

Senior debt holders are paid first and often have claims on company assets, leading to higher recovery rates in default scenarios.

2. What happens to equity investors during bankruptcy?

In most cases, equity investors are last in line and may lose their entire investment if the company cannot meet its obligations.

3. Should investors avoid lower positions in the capital stack?

Not necessarily. Lower-risk positions, such as equities, can offer higher long-term returns, but they should be balanced within a diversified portfolio aligned with risk tolerance.

About The Author

Brad Stark, MS, CFP®, is the Co-Founder and Chief Compliance Officer at Mission Wealth, where he plays a key role in guiding the firm’s strategic direction and long-term vision. As a member of the Leadership Team, Investment Committee, and Board of Directors, Brad works closely with advisors and clients to support thoughtful investment decisions and strong client outcomes. With decades of experience in the financial industry, he is passionate about helping individuals and families pursue their financial goals through disciplined planning, sound investment principles, and a client-first approach.

Customized Investment Management Solutions

At Mission Wealth, we develop customized, globally diversified, tax-efficient portfolios tailored to your financial plan and built to stand the test of time. Contact us below for a free portfolio review.Get Started Today

Investment Advice Fit For Your Needs

At Mission Wealth, we are deeply rooted in an evidence-based investment strategy built on decades of Nobel Prize-winning research. We ignore the media noise and Wall Street hype, relying instead on a long-term approach and proven principles that reward investors over time. For more information on Mission Wealth's investment strategies, please visit missionwealth.com.

To meet with a Mission Wealth financial advisor, please contact us online today or call us at (805) 882-2360.

Mission Wealth is a Registered Investment Advisor. This commentary reflects the personal opinions, viewpoints, and analyses of the Mission Wealth employees providing such comments. It should not be regarded as a description of advisory services provided by Mission Wealth or performance returns of any Mission Wealth client. The views reflected in the commentary are subject to change at any time without notice. Nothing in this commentary constitutes investment advice, performance data, or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Mission Wealth manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

00879205 03/26

Let's Keep in Touch!

Subscribe for exclusive content and timely tips to empower you on your financial journey. Our communications go straight into your inbox, so you'll never miss out on expert advice that can positively impact your life.Recent Investment Insights Articles

Market Update 3/19/26

March 19, 2026The Fed holds rates steady, balancing strong growth, oil price spikes, and geopolitical risks. Learn what this means for interest rates, inflation, and market outlook....

What Is the Capital Stack? How Investment Risk Changes from Debt to Equity

March 18, 2026Learn how the capital stack works and why your position, from senior debt to equity, determines risk, return, and recovery in downturns....

Why Investors Sell Too Early (or Too Late): 4 Behavioral Biases to Know

March 18, 2026Many investors focus on what investments to buy, but knowing when to sell is just as important. Learn four behavioral biases that influence selling decisions....