Year-end Tax Insights!

Mission Wealth Market Update for 3/3/23

Outlook

Current dynamics continue to support our outlook for tighter monetary policies over the foreseeable future: whereas the years post-GFC through 2021 were marked by easy policies (low interest rates and quantitative easing), expect the forthcoming period to be marked by higher interest rates and quantitative tightening. What does that mean for stocks? Long-term stock market returns are likely to moderate and fall in line with historic norms of mid- to high-single digit returns. We are constructive on the outlook for bonds, with many of our bond funds offering attractive yield opportunities in the current environment. We believe alternative income-oriented strategies may offer upside potential with little correlation to the broad stock market.

Ultimately, we believe our portfolios are well positioned to navigate the forthcoming period and continue to meet the long-term financial goals of our clients.

Market Update

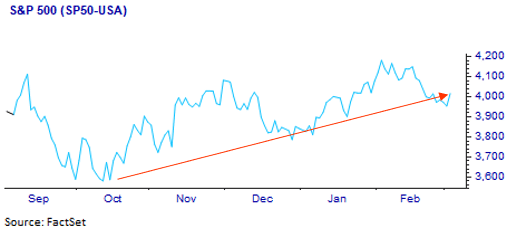

Markets have started the year positively, albeit giving up some of their momentum recently. Rising possibilities for a “soft landing” or “no landing” scenario combined with moderating inflation data helped sentiment earlier in the year, while more recent Fed interest rate repricing has since led to some softening. Through the end of February, the S&P was up +3.7%, while international stocks fared slightly better, with MSCI All World ex US Index up +4.4%. Despite some recent moderation, the S&P now sits more than 10% above its low in October of last year. Upwardly revised Fed policy expectations also led to an increase in interest rates, with the benchmark 10-year US Treasury yield currently trading above 4.0%, up from 3.5% at the end of January.

Expectations Rise for Fed Rate Hikes

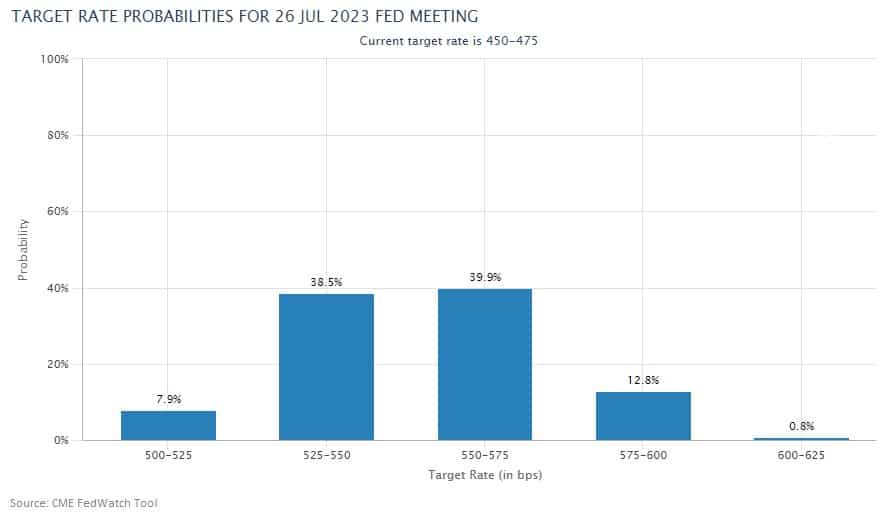

The recent upward repricing of Fed interest rate hikes has been a dominant market theme. After the Fed raised rates another 0.25% at the beginning of February amid a backdrop of moderating inflation data, cracks subsequently emerged in the disinflationary narrative. Stronger than anticipated January Producer Price Index (PPI) and core Personal Consumption Expenditures (PCE) data, along with a consistent “higher-for-longer” messaging from policymakers, including mentions of a 0.50% rate hike possibility, all pushed market expectations for the Fed's terminal rate higher, with little chance of a rate cut this year. Current probabilities indicate a greater than 50% chance the fed funds target will be 5.50%-5.75% or higher by July, inferring another 1% of fed funds rate increases (equates to a 0.25% increase at each of the four meetings through July).

No Cuts Likely

Contributing to this outlook is economic data, which continues to be robust and increasingly supportive of a “soft-landing” or more recently, a “no-landing” economic outcome. Notable economic releases included a very strong retail sales report, better than expected services sector data, a big beat for January nonfarm payrolls, and consistently low readings for initial jobless claims. With elevated and sticky inflation above the Fed’s long-term target of 2% and economic data pointing towards a soft-landing / no-landing outcome, we would need to see a significant deterioration in economic fundamentals before the Fed would even consider cutting rates. We just don’t see that unfolding over the near term.

Copyright © 2023, Mission Wealth is a Registered Investment Advisor. All rights reserved.

MISSION WEALTH IS A REGISTERED INVESTMENT ADVISER. THIS DOCUMENT IS SOLELY FOR INFORMATIONAL PURPOSES, NO INVESTMENTS ARE RECOMMENDED. ADVISORY SERVICES ARE ONLY OFFERED TO CLIENTS OR PROSPECTIVE CLIENTS WHERE MISSION WEALTH AND ITS REPRESENTATIVES ARE PROPERLY LICENSED OR EXEMPT FROM LICENSURE. NO ADVICE MAY BE RENDERED BY MISSION WEALTH UNLESS A CLIENT SERVICE AGREEMENT IS IN PLACE.

00501160 03/23