Year-end Tax Insights!

Mission Wealth Economic Update 7/22/2022

Overview

- The risk of a recession has weighed on markets recently, and there is a chance we experience two consecutive quarters of negative real GDP growth. In such an instance, the National Bureau of Economic Research (NBER) may find it hard to deem the current decline a recession when many other economic measures the NBER takes into account are pointing to expansion, not contraction.

- If deemed a recession, it would be a strange one, with exceedingly strong nominal growth, a very strong labor market and most economic data pointing up, not down.

- While a near-term recession is not our base case, if one comes to pass we anticipate it would be relatively mild. The economy has not built up significant excesses and certainly does not exhibit anywhere near the level of excesses witnessed ahead of 2008.

- We are constructive on the outlook for stocks from current levels and believe bond yields are likely to be range bound, with the current yield being the primary determinant of future bond returns.

- We continue to monitor developments closely and believe our portfolios are well positioned to navigate the current and forthcoming environment and will continue to meet the long-term goals of our clients.

Economic Update - Recession Risks Elevated

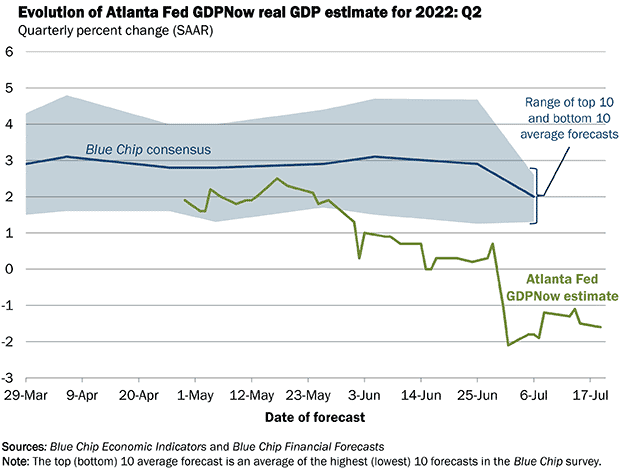

With slowing economic growth and a Fed determined to raise rates to combat inflation, the likelihood of a recession – driven by policy mistake or other – has increased. All eyes will be on next week’s preliminary estimate for second quarter real GDP growth, set for release on Thursday, 7/28 (it’ll be a busy week for economic data, with the Fed’s Federal Open Market Committee (FOMC) statement due out Wednesday, 7/27). There’s a chance the report will show two consecutive quarters of decline (Q1 real GDP fell -1.6%). Indeed, the Atlanta Fed’s GDPNow forecasting model has never been so closely followed and is currently pointing to a decline in second quarter real GDP of -1.6%.

On the other hand, consensus expectations are for real GDP to rise +1.5% in Q2. Nonetheless, there is a chance that the economy experiences two consecutive quarters of real GDP contraction. Will that mean we’re in a recession already? Not so fast.

Many Measures of the Economy Still Positive

If deemed a recession, it would be a very strange one. For one, the labor market is exceedingly strong, with the unemployment rate dropping from 3.9% to 3.6% this year and nonfarm payrolls continuing to climb in June, exceeding expectations. The pace of job growth has been robust all year, which is not consistent with how most people think of a recession. To this end, the National Bureau of Economic Research (NBER) – which is responsible for officially identifying economic expansions and recessions – emphasize several economy-wide measures of economic activity in making its assessment. Most of these inputs are showing continued economic growth, not decline.

These measures include:

- Real personal income, which hit an all-time high in May.

- Employment data: nonfarm payrolls jobs continued to climb in June, exceeding expectations and the unemployment rate has dropped to 3.6%.

- Real personal consumption expenditures, which experienced a decline in May after hitting an all-time high in April, though is still up 2.1% over the prior 12-months.

- Retail sales, which have increased 8.1% in the last 12 months through May.

- Industrial production, which hit an all-time high in May.

Additionally, NBER considers both gross domestic product (GDP) and gross domestic income (GDI) as key inputs in determining economic cycles. GDI increased +2.5% in the first quarter to reach an all-time high and was up 11.9% over the prior 12 months. Nominal GDP (that is unadjusted for inflation) continues to grow at a fast pace: over the last four quarters, nominal U.S. GDP growth averaged 12.2% and will likely be close to 10% for the balance of this year.

Regardless, the NBER won’t make a call overnight; the organization takes months to make an official determination. If officially deemed a recession, it would be a very weird one – at least by historic standards. One with exceedingly strong nominal growth, and most economic metrics pointing up, not down. Of course, if Q2 real GDP comes in-line with consensus expectations for a positive print there is unlikely to be any debate regarding an official economic contraction.

...But Economic Growth Appears to be Slowing

To be sure, economic growth appears to be slowing, not in small part due to the Fed which has raised rates to counter inflation. Consequently, financial conditions have become much tighter, while inflation has weighed on consumer confidence, which is at historic lows. Many high-profile companies have announced plans to slow hiring, which may cool the very hot labor market. The weakness in broad public markets has also contributed negatively to the wealth effect. Still, most economic metrics point to expansion, not contraction, albeit at a slower pace.

Next Recession Likely to be Mild

While our base case is that a recession won’t occur over the near term, if one does occur we think it would be a mild one, particularly in comparison to the two prior instances (the Global Financial Crisis of 2008 and the COVID-led recession of 2020). Both of which can be considered “once in a lifetime” events. Notwithstanding, these experiences remain fresh in the minds of many investors and may have factored into the recent market sell-off: the very hint of a recession leads some to flashbacks of the depths of the GFC. However, the reality is we currently don’t have anywhere near the level of excesses built up in the economy as we did back then, and it’s those excesses that tend to drive the worst recessionary periods. In contrast to 2008, consumers and corporations are in a much healthier situation.

Constructive on the Outlook for Stocks and Bonds

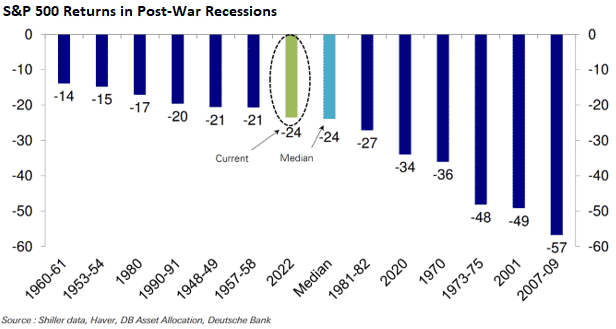

With this backdrop, we think there is more upside than downside for the stock market from current levels. The magnitude of the recent sell-off is in-line with the median recession-driven selloffs of the post-war era, so even if a recession were to transpire (again, not our base case), the market appears to have already priced it in. As such, we don’t anticipate material downside from current levels. If, on the other hand, we experience continued – albeit slowing – economic growth, this may act as a tailwind for stocks moving forward. The historically large increase in company announced stock buybacks is worth noting, which may help to underpin the stock market moving forward.

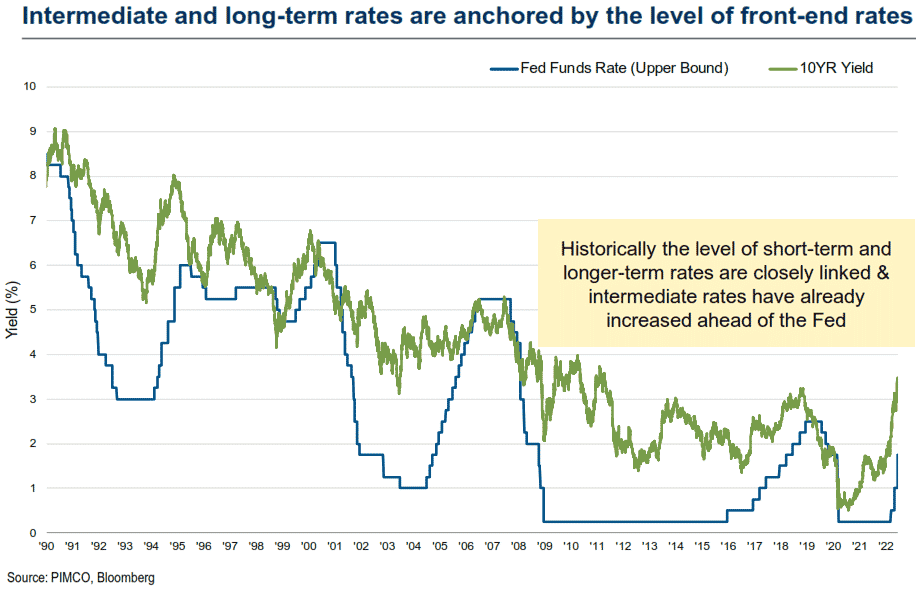

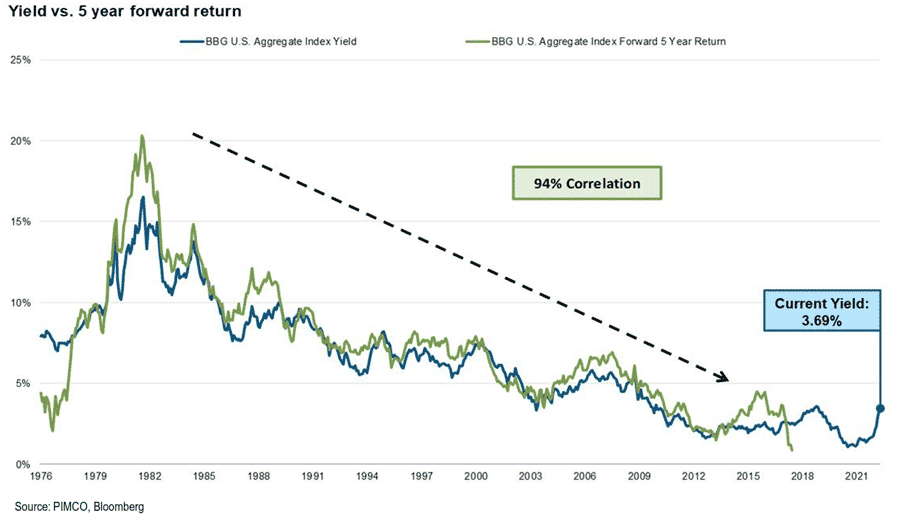

We believe bonds yields are likely to stay in a range-bound pattern, and therefore the pain may largely be behind us for bond returns. While ongoing uncertainty surrounding the economy and Fed policy may cause bond prices to fluctuate somewhat, we anticipate the primary determinant of future returns is the current yield on bond portfolios. The broad bond market – as measured by the benchmark Bloomberg US Aggregate Bond Index – is currently yielding 3.7% and many of our preferred income-oriented funds are offering much more attractive current yield profiles.

We continue to monitor macroeconomic data and developments closely. We believe our portfolios are well positioned to navigate the current and future environment, providing consistent income and growth potential to ultimately achieve our client’s financial goals.

As always, should you have any questions, please don’t hesitate to contact your client advisor.

ALL INFORMATION HEREIN HAS BEEN PREPARED SOLELY FOR INFORMATIONAL PURPOSES. ADVISORY SERVICES ARE ONLY OFFERED TO CLIENTS OR PROSPECTIVE CLIENTS WHERE MISSION WEALTH AND ITS REPRESENTATIVES ARE PROPERLY LICENSED OR EXEMPT FROM LICENSURE. PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RETURNS. INVESTING INVOLVES RISK AND POSSIBLE LOSS OF PRINCIPAL CAPITAL. NO ADVICE MAY BE RENDERED BY MISSION WEALTH UNLESS A CLIENT SERVICE AGREEMENT IS IN PLACE.

MISSION WEALTH IS A REGISTERED INVESTMENT ADVISER. THIS DOCUMENT IS SOLELY FOR INFORMATIONAL PURPOSES, NO INVESTMENTS ARE RECOMMENDED.

00458286 07/22